Customer Care: 866.625.8532 Sales Inquiries: 503.419.3544

CarePayment Named Top Performer in Patient Financing and Financial Engagement Solutions by Black Book Research - Read Press Release

Blog | February 4, 2021

How Patient Financing Can Aid in Improving Health Equity

Healthcare organizations have worked diligently to care for employees and patients during the pandemic. As healthcare workers strive to flatten the curve and prepare for widespread vaccine distribution, the pandemic continues to stress our health systems and bring matters of public health to the forefront. In particular, COVID-19 has underscored inequities and financial barriers to care that already existed within this system.

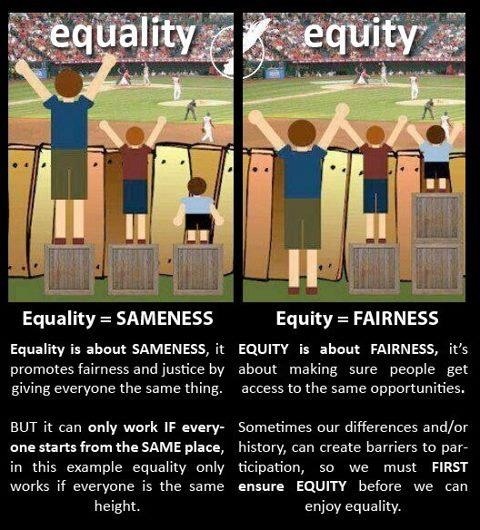

Health Inequity

The World Health Organization (WHO) defines health equity as “the absence of unfair and avoidable or remediable differences in health among population groups defined socially, economically, demographically or geographically.” For this to be achieved, not only do immediate inequities need to be addressed, such as access to resources and care, but also legislation and social norms that create those obstacles must be amended to make sure health is protected as a human right. This is not to be confused with “inequality,” which implies a lack of sameness. This scenario presents a lack of fairness and access to the same opportunities.

In December, CarePayment sponsored a Leadership Health Care Lunch & Learn titled, “Understanding & Addressing Social Determinants of Health to Optimize Behavioral & Health Equity.” The speaker, Dr. Bryan Heckman, Director of the Center for the Study of Social Determinants of Health and Associate Professor at Meharry Medical College discussed the many challenges facing vulnerable populations in seeking health equity.

According to Heckman, health equity requires that everyone has the opportunity to attain his or her full health potential through equal access to quality education, healthcare, housing and transportation with equal employment and income opportunities void of discrimination.

Unfortunately, progress has been slow. The Journal of the American Medical Association analyzed trends in health equity from 1993-2017 and found that not much progress has been made in the past 25 years in the United States. The takeaway is that public health policymakers, health systems and the healthcare industry as a whole need to work together to better address the inequities in this country regarding health.

How is COVID-19 affecting Vulnerable Populations?

The lack of progress has never been more evident as it is amid the pandemic. Vulnerable populations — those that are largely non-white with a median income of $60,240 or less — are not only eight times more likely to be infected by COVID-19, but they are also nine times more likely to die due to the complications associated with the disease, according to a research letter published in the JAMA Network Open.

On top of that, in 16 states that have released data by race, white residents are being vaccinated two to three times more than Black residents, as Kaiser Health News has reported. As the world turns the corner on COVID-19, a concerning trend is emerging.

How does the Patient Financing Industry Play a Role in Health Equity?

The relationship between health equity, COVID-19 and financial barriers to healthcare are inseparable. While health systems throughout the country address equitable patient access to quality healthcare, the challenges are highlighted by the pandemic. The financial experience for patients is often overlooked as part of the equation and can inadvertently exacerbate inequities.

So, what role does someone in revenue cycle management, specifically patient access, play in reversing the trends and reducing health inequity? While individuals in patient financing cannot possibly address the many challenges our country faces, we can help in the effort to build a more equitable society.

Through a combination of a robust financial assistance program and no-application, zero-interest patient financing, health systems can make healthcare that much more financially attainable for everyone, regardless of socioeconomic status. When offered in a fair and compassionate manner, patient financing can help vulnerable populations get the care they need.

However, not all patient financing plans are created equally. Many plans require credit checks and high credit scores to qualify, which tends to exclude people who need the most help. And if they’re not turned away, they’re subjected to high interest rates that can take years to pay off.

Credit scores can highlight inequities and perpetuate socioeconomic disparities, which affects more than just the people who are struggling financially but also the cities in which they live. According to the Urban Institute, 38 of the 60 (major US) cities have differences in median credit scores of 100 points or more between predominantly white and non-white areas. Nationally, the difference in median credit scores is nearly 80 points, which can cost families thousands of dollars over the life of the loan.

CarePayment is a comprehensive solution that does not require a credit check or an application. All patients who need help with out-of-pocket medical expenses qualify for our program. Patients simply tell their provider they’re interested in a CarePayment plan, make their first payment and they’re enrolled. Patients also have the ability to add future charges to their CarePayment account at any time.

In addition, part of reducing inequity is increasing awareness of resources that are available. Through our partnerships with health systems and providers, we’re able to engage patients before they even realize they need help. Meaning, those who don’t know to ask are not barred from getting financial assistance.

Other solutions that require credit checks have an application process that can be lengthy, and if a patient needs another loan for medical care down the road, they’ll have to repeat the application process.

Because CarePayment does not require a credit check, we are able to offer interest-free financing. This is not an introductory offer or deferred interest plan, often offered to patients based on credit scores. These plans disproportionally affect patients with lower credit scores and can add hundreds of dollars to a balance and lead to increased loan defaults. CarePayment is always 0.00% APR over the life of the financing.

While COVID-19 has highlighted many of the inequities in our health systems, which will take a combined effort between policy makers and healthcare providers to correct, there are ways to contribute to a more complete system now by offering compassionate and fair financing solutions that deliver more patient payments.

Drake Jarman is a Regional Vice President for CarePayment and works with hospitals and health systems to improve revenue and the patient financial experience. For over 15 years, Drake has helped providers find innovative ways to use data, technology, and subject matter expertise to improve operations. To learn more, reach out to drake.jarman@carepayment.com to discuss challenges in revenue cycle and strategies for patient financing.

{kind=link}

CarePayment Integrated Engagement Platform

Beacon Health Provider Story

Client Testimonial: The Right Partner

Comprehensive Patient Financing